Geopolitical risk and continuous disclosure: how ASX 200 entities are responding to the Iran conflict

30 April 2026

Updated 1 May 2026

The Iran conflict has sent shockwaves through energy, commodity and financial markets. With regulators and shareholders growing increasingly willing to hold listed entities to account, the pressure on listed entities to get continuous disclosure right has never been greater, particularly in the case of forward-looking guidance. This article provides an overview of the continuous disclosure regime and reviews ASX 200 entities’ continuous disclosure activity since the Iran conflict escalated on 28 February until 1 May 2026. The results of the review reveal interesting insights into how listed entities are responding to the conflict which may be of interest to ASX boards, general counsel and investor relations teams.

Continuous disclosure regime

Statutory framework

A listed entity’s continuous disclosure obligations are set out in the Corporations Act 2001 (Cth) (section 674) and ASX Listing Rules (Listing Rule 3.1). In short, if a listed entity becomes aware of information that a reasonable person would expect to have a material effect on the price or value of its securities, it must immediately disclose that information to ASX, subject to certain exceptions.

For forward-looking guidance specifically, if an entity becomes aware that its guidance will differ materially from market expectations – whether upwards or downwards – and that difference would be material to price or value, then the entity must update or withdraw the guidance.

Recent case law on guidance

In our recent Insight, we discussed practical lessons from the recent Federal Court decision in Southernwood v Brambles Limited (No 3) [2026] FCA 418 (Brambles).

Key takeaways include:

- earnings guidance should be subject to continual reassessment, not merely initial verification;

- management assumptions and recovery plans should be critically tested against actual performance to ensure that they remain objectively supportable;

- boards should ensure that robust governance and escalation processes exist around disclosure decisions;

- optimism and aspirational forecasting, without objective support, may not withstand regulatory and judicial scrutiny; and

- the existence of a ‘reasonable basis’ must be reassessed continuously – it may diminish as contrary information emerges.

In the context of the Iran conflict, listed entities should therefore be continually testing whether the assumptions underpinning their guidance remain reasonably supportable. If a ‘reasonable basis’ ceases to exist for particular guidance, then that guidance should be revised, withdrawn or qualified. We wouldn’t be surprised if the Brambles decision results in litigation funders sharpening their focus on potential shareholder class actions relating to guidance and disclosure.

ASX guidance on continuous disclosure and the Iran conflict

ASX has published Guidance Note 8 to assist listed entities with understanding and complying with their continuous disclosure obligations. The Guidance Note includes specific guidance on earnings guidance and market sensitive earnings surprises (see sections 7.1 and 7.3).

On 9 April 2026, ASX issued a compliance update acknowledging that the evolving nature of the Iran conflict may create disclosure challenges for listed entities and affects them differently. It provided guidance regarding continuous disclosure and the Iran conflict (ASX Compliance Update no. 02/26) which included:

- Continuous disclosure does not require ‘predicting the unpredictable’.

- ASX does not expect entities to announce matters of supposition or information that is insufficiently definite to warrant disclosure, or that otherwise falls within the Listing Rule exceptions.

- Entities should not make forward-looking statements unless they have a clear and reasonable basis to do so. Such guidance already made by entities that are potentially affected by the Iran conflict must be actively reviewed and revised.

- An entity would not generally be expected to disclose publicly available information about external events affecting all entities in the market, or a particular sector, in the same way.

- However, if the conflict is likely to cause an entity’s earnings to differ materially from previously issued guidance, then that information must be disclosed. Similarly, any operational decision likely to have a material effect on price or value – for example, a decision materially impacting the level of ongoing operations – must be announced immediately.

The upshot is this: a listed entity is not required to speculate about the trajectory of the conflict. However, once it has released forward-looking guidance, it must inform the market of any material changes to that guidance and any operational decisions likely to have a material effect on price or value.

Consequences of failing to comply

Listed entities face the risk of regulatory enforcement action by ASX and ASIC for breaching continuous disclosure obligations. Enforcement may also include an action for misleading or deceptive conduct (section 1041H of the Corporations Act 2001 (Cth) and section 12DA of the Australian Securities and Investments Commission Act 2001 (Cth)) and result in suspension from the ASX, issuing of infringement notices, commencement of civil penalty proceedings and, in serious cases, criminal prosecution.

Listed entities may also be exposed to shareholder class actions for non-compliance with continuous disclosure obligations. Shareholders (and litigation funders) are increasingly willing to scrutinise the basis on which guidance was issued or maintained, as illustrated by Brambles.

Non-compliance may also cause significant reputational damage for the listed entity, which in turn can impact share price, access to capital and stakeholder relationships.

Review of ASX 200 entities’ Iran conflict disclosures

Methodology

We reviewed ASX 200 entities’ market announcements between 28 February 2026 and 1 May 20261 to identify ASX announcements that contained keyword references to the Iran conflict, including terms such as ‘Iran’, ‘Hormuz’, ‘Middle East’ and related expressions. Our review identified 123 ASX announcements published by 71 ASX 200 entities.2

Each of the 123 announcements was then individually reviewed to assess the nature and depth of the Iran conflict reference – distinguishing between substantive disclosures and incidental disclosures.

Disclosures were classified as:

‘substantive’ if they quantified an operational or financial impact, revised previous earnings guidance, disclosed exposure to its operations, costs or supply chain or made commercial or strategic commentary impacting the entity’s business, due to the Iran conflict; and

‘incidental’ if the conflict reference was limited to general market commentary without any specific impact to the entity’s business or operations being identified.

Timing of the announcements, industries/sectors in which entities were making announcements and whether there were any key trends/themes across announcements was also considered.

Key findings

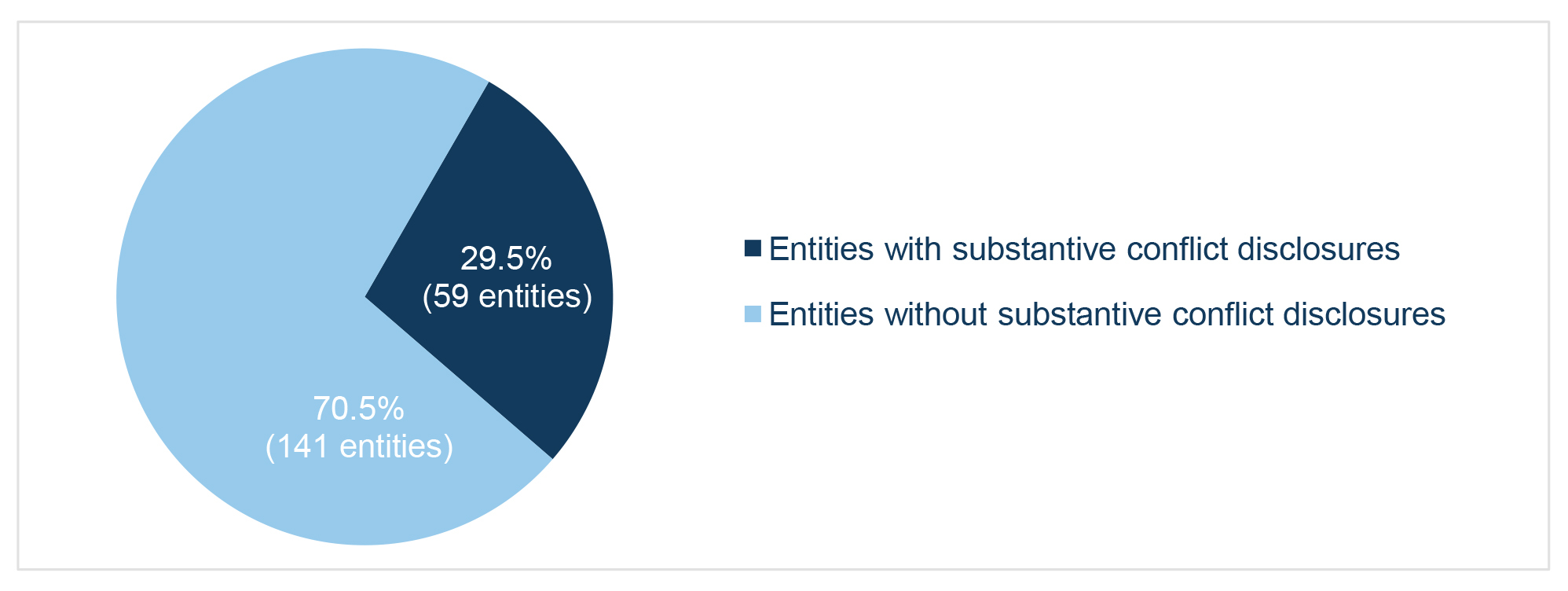

Energy and Resources entities dominate disclosures

Only 59 (29.5%) of ASX 200 entities have made substantive disclosures referencing or responding to the Iran conflict. 31 of these entities (52.5% of disclosers) operate in the Energy & Resources sector.3 The remaining 29 entities span a range of sectors, including Capital Markets (6 entities), Transportation Infrastructure (3 entities), Banks (6 entities) and various other sectors.4

Chart 1: Proportion of ASX 200 entities making substantive Iran conflict disclosures

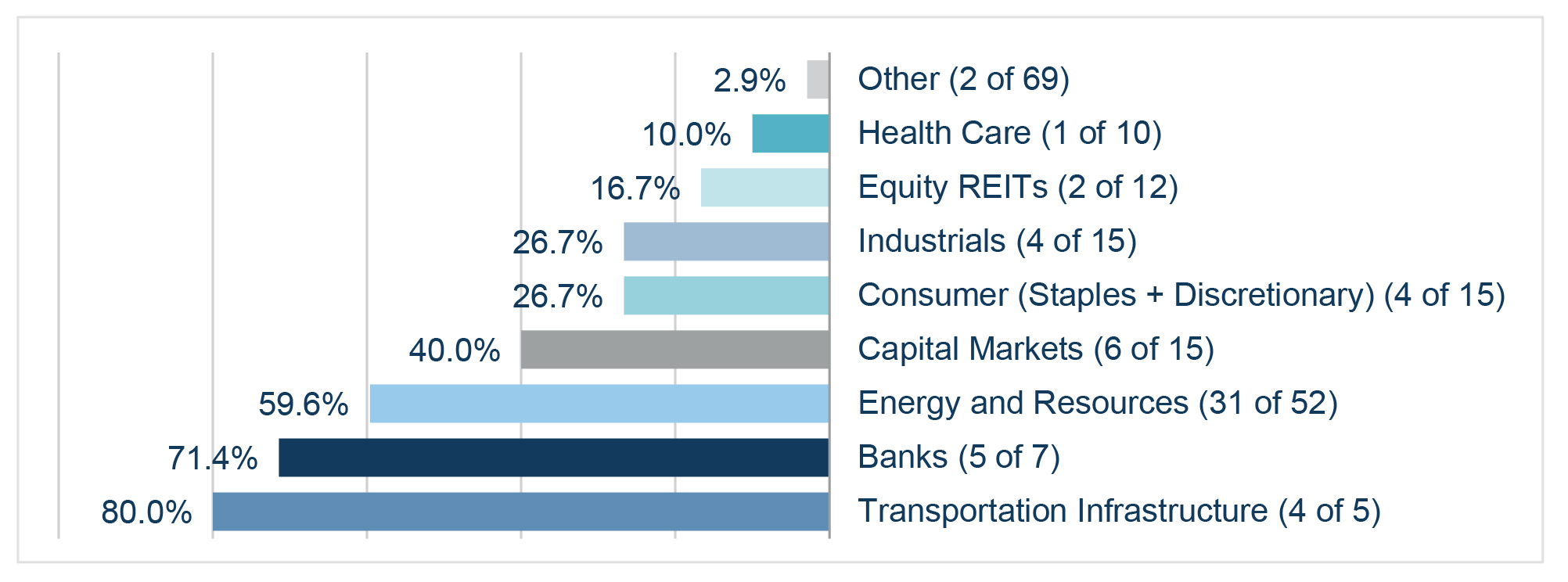

Highest rate of substantive disclosure in the Transportation Infrastructure, Banks and Energy & Resources sectors

Review of substantive disclosure rates by industry sector reveals that the highest disclosing sectors were Transportation Infrastructure (80%), Banks (71.4%) and Energy & Resources (59.6%). Disclosure rates in other sectors range from 2.9% to 40%. Only one entity in the Health Care sector made a substantive disclosure while no substantive disclosures were made by entities in the Communication Services sector.

Chart 2: Sector disclosure rate – percentage of ASX 200 entities in each sector making substantive disclosures

Iran conflict-related matters covered in substantive disclosures include:

supply chain risks for key inputs;

pricing and availability of fuel and diesel;

shipping and freight disruption;

operational disruption;

reduced sales;

elevated commodity prices and refining margins; and

credit provisioning for exposed sectors.

A consistent theme in the substantive disclosures made by Energy & Resources entities was that physical diesel supply remained uninterrupted at the time of disclosure, with the primary concern being the cost impact of higher prices rather than availability. Certain entities in other sectors disclosed positive impacts, including elevated margins and higher commodity prices.

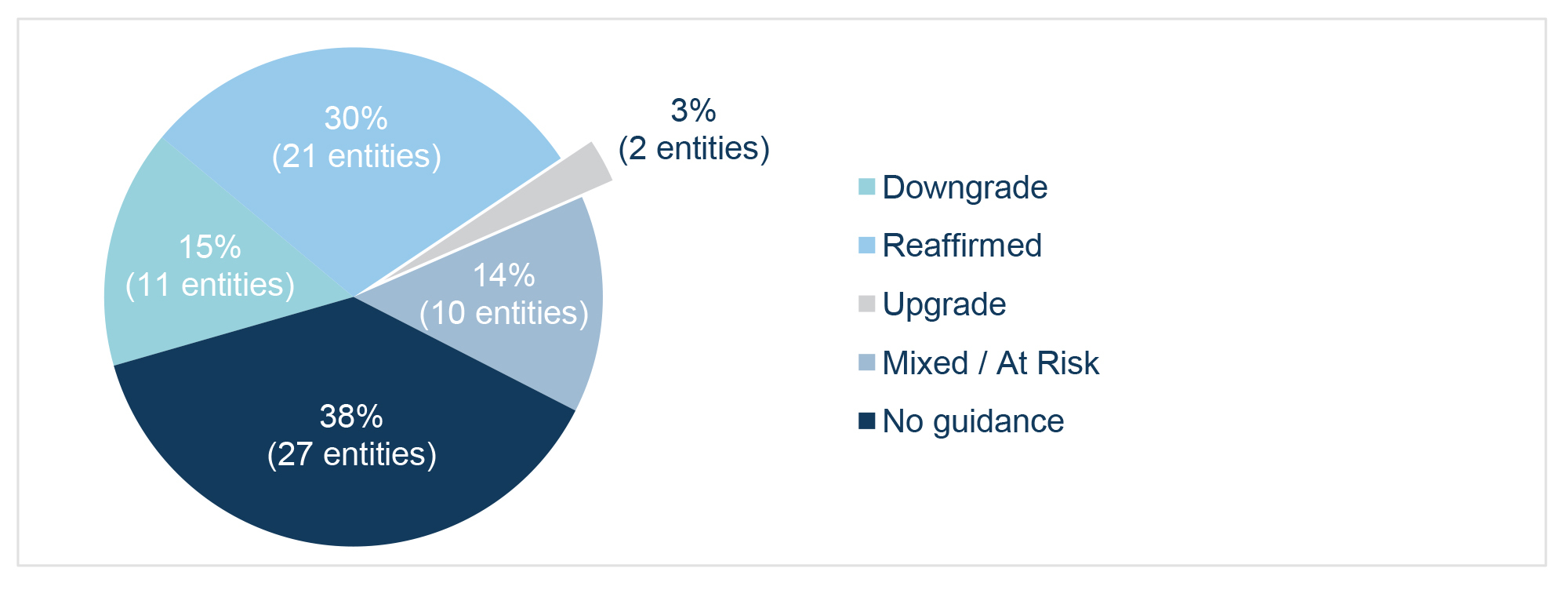

Guidance reaffirmation most common; notable downgrades

Of the 71 entities that published the 123 ASX announcements, 44 (62%) entities addressed earnings guidance in some form – 21 reaffirmed existing guidance, 11 issued downgrades (or disclosed conflict-related earnings impacts), 2 issued upgrades, and 10 provided mixed or ‘at risk’ guidance (where guidance was retained but explicitly conditioned on the conflict’s duration or severity). A further 27 (38%) entities discussed the conflict without issuing or revising formal earnings guidance.

Chart 3: Guidance responses among companies addressing the Iran conflict

The prevalence of reaffirmations suggests that entities not negatively impacted by the Iran conflict were eager to reassure the market that their outlook remains intact. Downgrades were driven by higher fuel and energy costs, supply chain disruption and freight cost escalation, reduced demand or order cancellations in conflict-affected regions, increased credit provisioning by banks and higher operating costs across operations. Several entities that had upgraded guidance likely benefited from elevated commodity prices driven by the conflict. Where guidance was issued with little margin for error, as Brambles illustrates, the discipline required to support it is higher, not lower, as contrary information emerges.

Timing of disclosures

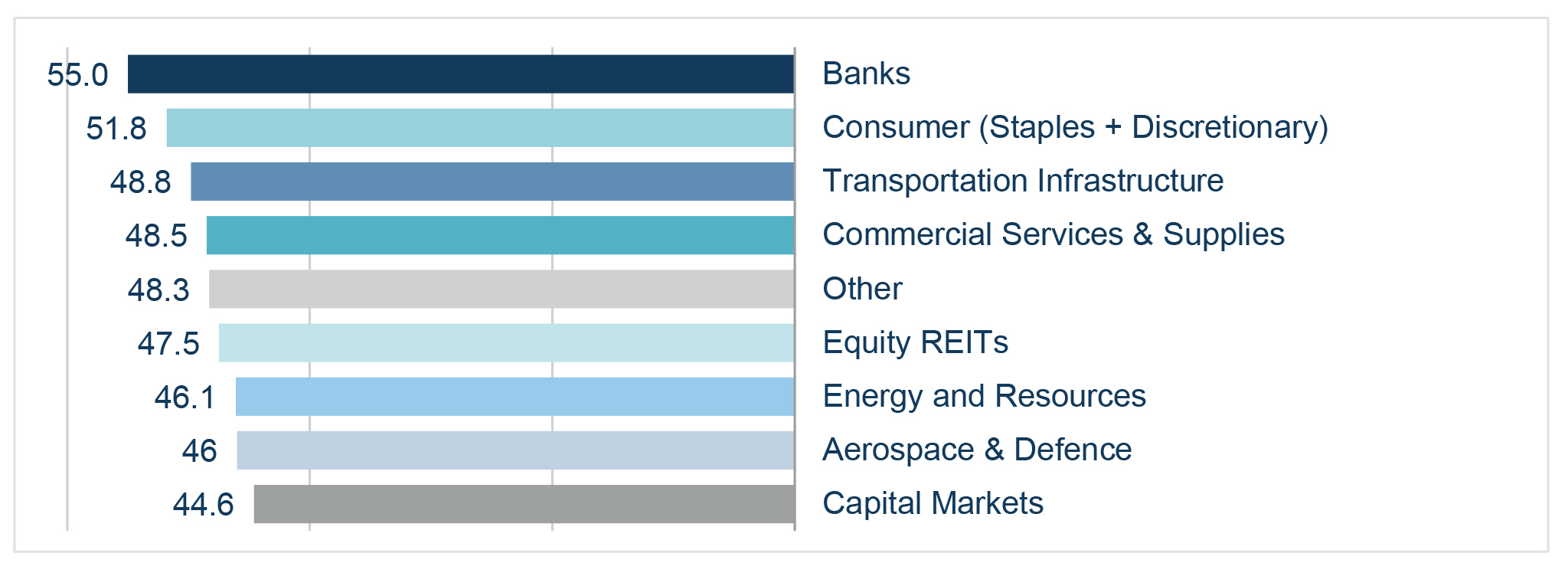

The average time from conflict escalation (28 February 2026) to a substantive disclosure was approximately 46 days, broadly aligned with the March quarterly reporting cycle for Energy & Resources companies and the April half-year reporting cycle for banks. The latest substantive disclosures were made approximately 62 days post-escalation. The bulk of disclosures fell in the 39–62 day window which interestingly followed ASX’s April guidance regarding continuous disclosure and the conflict.

Chart 4: Average days from 28 February 2026 to substantive disclosure by industry sector

The silent majority

70.5% of ASX 200 entities – including many of the largest by market capitalisation – have not made any substantive disclosures regarding the Iran conflict. This may reflect a view that the conflict’s impact is not yet material enough to warrant entity-specific disclosure, or that entities have been able to manage the operational impacts (such as fuel supply and pricing) without needing to update the market.

Possible drivers for not disclosing include the ability of large, diversified entities to absorb cost increases through existing procurement arrangements, and the absence of material direct operations, customers or suppliers in the Middle East. We expect that these entities are nonetheless closely monitoring the situation and will update the market as required, particularly when they have previously provided guidance. Entities that have provided guidance and have not yet disclosed should nonetheless be actively reassessing that guidance now and be prepared to act promptly if circumstances change.

Key takeaways

Geopolitical events like the Iran conflict test how well entities comply with continuous disclosure obligations, where getting it wrong can have significant consequences. Key takeaways include:

Continuous reassessment: Entities should conduct ongoing and regular review of the impacts of geopolitical events and promptly update or withdraw guidance where it is no longer current.

Disclosure exceptions: Where geopolitical events cause material impacts, withholding disclosure warrants careful consideration and should be appropriately documented.

Reasonable basis: Uncertainty does not diminish the requirement that any guidance must have a reasonable basis.

Regulatory and litigation risk: Disclosure decisions should be made on the expectation of regulatory scrutiny and potential shareholder claims.

[1] The initial review included over 2800 ASX announcements. Harvey (Legal AI platform) was used to assist with identifying relevant ASX announcements.

[2] ASX announcements that did not contain explicit keyword references to the Iran conflict and related terms but may have referred to macroeconomic factors arising from the conflict (eg. higher fuel costs, supply chain disruption) may not have been identified.

[3] ‘Energy & Resources’ refers to entities classified under the GICS industry codes of either ‘Metals & Mining’ or ‘Oil, Gas & Consumable Fuels’.

[4] ‘Other’ is comprised of single entities in the following industry sectors: Aerospace & Defence, Chemicals, Commercial Services & Supplies, Construction Materials, Diversified Financial Services, Electricity Utilities, Food Products, Health Care Equipment & Supplies, IT Services, Multi-Utilities and Passenger Airlines.

Authors

Tags

This publication is introductory in nature. Its content is current at the date of publication. It does not constitute legal advice and should not be relied upon as such. You should always obtain legal advice based on your specific circumstances before taking any action relating to matters covered by this publication. Some information may have been obtained from external sources, and we cannot guarantee the accuracy or currency of any such information.

Key Contact

Other Contacts